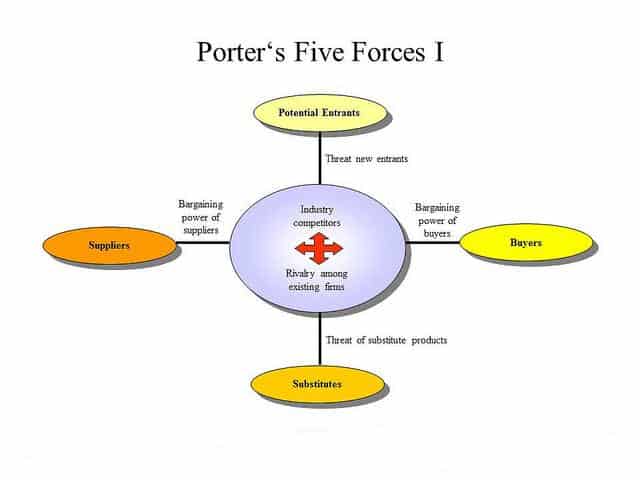

Porter’s Five Forces Model of Competitive Industry Structure

An industry is a group of firms that market product which are close substitutes of each other. Some industries are more profitable than others. But this difference cannot be totally explained by fact that one industry provides better customer satisfaction than others. There are other determinants of industry attractiveness and long run profitability, that shape the rules of competition. Porter’s five forces model of competitive industry structure adequately explains these forces.

Threat of New Entrants

New entrants raise the level of competition in an industry and reduce its attractiveness. Threat of new entrants depends on barriers to entry. More barriers to entry reduces the threat of new entrants. Some of the key entry barriers are:

Economies of scale – Industries where the fixed investment is high (such as automobiles), yield higher profits with larger scale of operations. In such industries, established players may have economies of scale of production which new entrants will not have, thus acting as a barrier.

Capital Requirements– Industries that require large seed capital for establishing the business (such as steel) discourage new entrants that cannot invest this amount.

Switching Costs – Customers may face some switching cost like having to buy new spare parts or train employees to run the new machine, in moving from one company to the other, thus discouraging movement of customers from existing players to new entrants.

Access to Distribution – Established players may have access to the most efficient distribution channels. Distribution channel members may not tie up with new entrants who pose competition to their existing partners.

Expected Retaliation – If existing players have large stakes in continuing their business large investment, substantial revenues,strategic importance), or if they are dominant players, they would retaliate strongly to any new entrant.

Brand Equity – Existing players have established product reputation and built a strong brand image over the years. New players would find it hard to convince customers to switch over to their offering.

Bargaining Power of Suppliers

Higher bargaining power of suppliers will mean higher costs for the companies in the industry. Bargaining power of suppliers will be high when:

Many Buyers and Few Sellers – There are many buyers and few dominant suppliers. Suppliers would be in a position to charge higher prices or cause instability in supply of essential products. The buyers should develop more suppliers by agreeing to invest in them and helping them with technologies.

Differentiated Supplies – When suppliers offer differentiated and highly valued components, their bargaining power is higher, since the buyer cannot switch suppliers easily. When many suppliers offer a standardized product, their bargaining power reduces. The buyer should bring the processes that enable the supplier to make differentiated products in-house and buy only standard components from the supplier.

Crucial Supplies – If the product sold by the supplier is a key component for the buyer, or it is crucial for its smooth operations, then the bargaining power of suppliers is higher. The buyer should always keep the production of key components with itself.

Forward Integration – When there is a threat of forward integration into the industry by the suppliers, their bargaining power is higher. There is a strong threat of forward integration when the supplier supplies a very crucial part of the final product. The supplier of engines to an automobile maker is in a very strong position to contemplate making automobiles because it already has expertise over a key component of the final product.

Backward Integration – When there is threat of backward integration by buyers, the bargaining power of suppliers becomes weaker, as the supplier may become redundant if the buyer starts making the same product. The buyer should always have idea of the technologies that are being employed in making crucial and differentiated products and should be capable of putting together the resources to make these components. Suppliers should always understand that if the buyer is cornered he will start making the components himself.

Level of Dependence – When the industry is not a key customer group for suppliers, their bargaining power increases. Buyers are dependent on suppliers, though suppliers do not focus on the customer group. The suppliers can survive even when they stop supplying to the buyers as the major part of their business is coming from some other industry. The buyers should be careful in selecting their suppliers. They should select suppliers who have strong stake in the buyers’ industry and not those who only have peripheral interests in the buyers’ industry.

A firm can reduce bargaining power of suppliers by seeking new sources of supply, threatening to integrate backward into supply, and designing standardized components so that many suppliers are capable of producing them.

Bargaining Power of Customers

Higher bargaining power of customers implies that they can seek greater compliance from the companies of the industry.

Few Dominant Customers – When there are few dominant customers and many sellers, customers can exercise greater choice. They also dictate terms and conditions to the supplier. This is true in industrial markets where many suppliers make standard components for a few Original Equipment Manufacturers.

The OEMs are able to extract big concessions on price and coerce the suppliers to provide expensive services like just-in-time supplies. The suppliers have to agree to debilitating terms of the buyers if they have to continue to supply to them.

Non-differentiated Products – If products sold by the players in the industry are standardized, or there are little differences, buyers can easily switch over to competitors, increasing their bargaining power. This is increasingly happening in consumer markets. Customers are not able to tell one manufacturer’s product from that of another. The result is that the customers are buying mostly on price and the manufacturers are reducing prices to lure customers.

Small Proportion of Customer’s Total Purchase – If the product offered by the firm is not important or critical for the customer, the bargaining power of customers is higher

Backward Integration -Customers may threaten to integrate backward into the industry, and compete with suppliers. This may be a reality in industrial markets but it is very rare in consumer markets. Most customers do not have the resources to start making what they buy.

Forward integration– Suppliers can threaten to integrate forward into customers’ industry. The customers have to understand and contain the imminent threat of competition from their suppliers. This threat is meaningless in consumer markets but the threat is real in industrial markets, particularly when the supplier is supplying a key component.

Key Supplies – The industry is not a key supplying group for buyers. In consumer markets, one manufacturer supplies only a small fraction of his total purchases.

Firms in the industry can attempt to lower buyer power by increasing the number of buyers they sell to, threatening to integrate forward into the buyer’s industry and producing highly valued differentiated products.

Threat of Substitutes

Presence of substitute products can lower industry attractiveness and profitability because they put a constraint on price levels. They also widen the scope of competition and present more alternatives for the buyer. Raising price of coffee would make tea more attractive. The threat of substitute products depends on:

Buyer’s willingness to substitute– Buyers will substitute when the industry’s product is not strongly differentiated. In industrial markets, the product should either enhance value of the final product it becomes o part of or enhance the operation of the buyer.

Relative Prices and Performance of Substitutes – If the substitute enhances the operation of the customer without incurring additional costs, a substitute product would be preferred.

Costs of Switching Over to Substitutes – In industrial markets if a company has to buy another manufacturer’s product, the company will have to buy new spare parts and will have to train its operations and maintenance staff on the new machine.

Industry Competitors

The intensity of rivalry between competitors depends on:

Structure of Competition – More intense rivalry prevails when there are a large number of small competitors or a few equally balanced competitors. There is lesser rivalry when a clear leader (at least 50% larger than second) exists with a large cost advantage.

Structure of Costs – High fixed costs encourage price cutting to fill capacity. This may be matched by competitors resulting in a price war.

Degree of Differentiation – Commodity products encourage rivalry while highly differentiated products which are hard to copy are associated with less intense rivalry

Switching Costs – When switching costs are high because product is specialized, and the customer has invested a lot in resources in learning how to use the product or has made tailor made investments that are worthless with other products and suppliers, rivalry is reduced.

Strategic Objectives – When competitors are pursuing build strategies, competition is more intense than when playing hold or harvest strategies.

Exit Barriers – When barriers to leaving an industry are high due to such factors as lack of opportunities elsewhere, high vertical integration, emotional barriers or high cost of closing down plant, rivalry will be more intense than when exit barriers are low.